SBA Raises Loan Limits to $10M

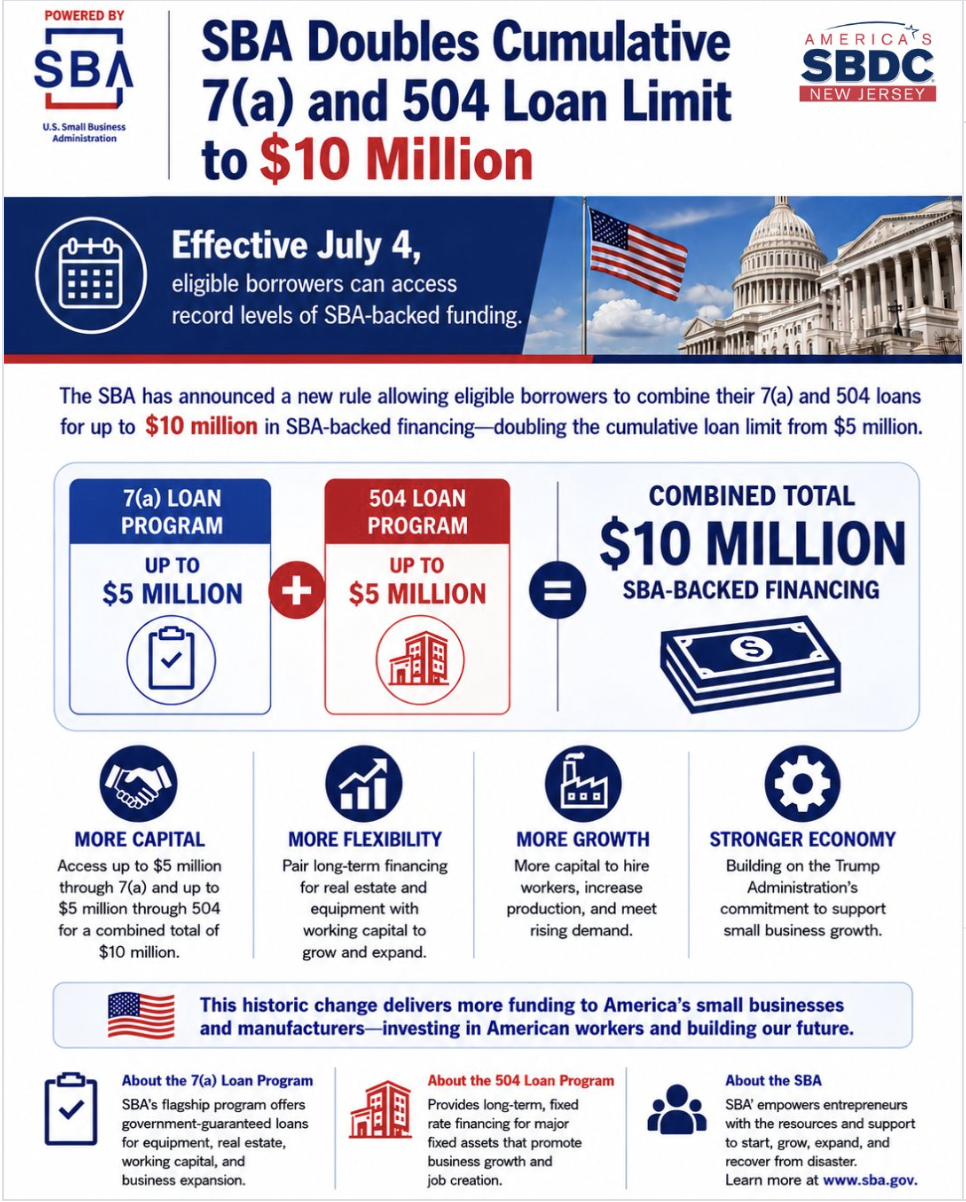

The U.S. Small Business Administration has expanded one of its most important financing tools. As of May 2026, the SBA doubled the cumulative borrowing limit for its 7(a) and 504 loan programs to $10 million.

This is not a small policy adjustment. It changes how small and mid-sized businesses can think about growth, expansion, and long-term planning.

For many companies, access to capital has been the limiting factor. This update removes part of that ceiling.

What Actually Changed in the Loan Structure

Previously, businesses using SBA-backed loans were limited in how much they could borrow across multiple loans. Even if a company qualified financially, it could hit a cap that restricted further expansion.

With the new update, businesses can now access up to $10 million in total SBA-backed financing across the 7(a) and 504 programs.

This matters for companies that are growing in phases. Instead of securing one loan and stopping, they can now layer financing over time as they expand operations, invest in equipment, or enter new markets.

The structure now better reflects how businesses actually grow.

Why This Matters for Growing Businesses

Growth rarely happens all at once. Businesses expand in stages. They hire, invest, upgrade systems, and increase capacity gradually.

Under the previous limits, many companies reached a point where financing options became restricted just as they were gaining momentum. They had demand. They had customers. But they lacked the capital to scale. This update changes that.

Businesses that are ready to move beyond early-stage operations into full-scale growth now have more room to do so. That includes:

expanding facilities

purchasing large equipment

opening additional locations

investing in production or logistics

entering new regional or national markets

The difference is not just access to money. It is access to continuity.

From Small Business to Scalable Business

This policy shift signals something larger. The SBA is no longer focused only on helping businesses start. It is placing more emphasis on helping them scale. There is a difference between a small business and a scalable business. A small business operates efficiently within its limits. A scalable business grows beyond them. The increased loan cap allows businesses to move into that second category. It supports companies that are ready to transition from steady operation into expansion mode. This is especially important in industries like manufacturing, healthcare, logistics, and construction, where growth often requires significant upfront investment.

How This Connects to Current Economic Trends

The timing of this update matters. Across the U.S., businesses are facing rising costs, workforce challenges, and increasing competition. At the same time, there are strong opportunities tied to domestic production, infrastructure investment, and regional growth. In Texas, this is especially visible. The state continues to attract major business projects, but small and mid-sized companies must scale quickly to participate in that growth. Without access to capital, they risk being left out. With expanded loan limits, more businesses can position themselves to take on larger contracts, meet higher demand, and compete in a changing market.

Capital Alone Is Not Enough

Access to funding is critical, but it does not guarantee success. Businesses that take on larger loans must also have:

strong operational systems

clear financial planning

defined growth strategies

capacity to manage expansion

The risk is not the loan itself. It is scaling without structure. Companies that use this opportunity effectively will align financing with strategy. They will invest in areas that generate long-term returns, not just short-term growth.

What Businesses Should Consider Right Now

This update creates opportunity, but it also raises expectations.

Business owners should start asking:

Is the company ready to scale beyond its current size?

Are there systems in place to support growth?

What investments would actually increase capacity or revenue?

Is financing being used strategically or reactively?

The businesses that benefit most will be the ones that plan ahead, not the ones that borrow without direction.

A Shift Toward Larger, Stronger Small Businesses

The SBA’s decision reflects a broader trend in the economy. Small businesses are being asked to do more. They are expected to compete at higher levels, integrate technology faster, and respond to larger market opportunities. This requires more capital. By increasing the loan limit, the SBA is acknowledging that the definition of “small business” is evolving. Many companies fall between traditional small businesses and large enterprises. They need tools that match that position. This update is one of those tools.

Turning Access Into Strategy

Access to capital is only the first step. Knowing how to use it is what creates impact. Through our work at Emerge and Rise and our partnerships, we help businesses understand funding options, align them with growth strategies, and build the systems needed to scale responsibly. If your business is considering expansion, now is the time to evaluate what this new loan capacity could mean for your next phase. Connect with us!

Your donations make our work possible.

When you give to Impact, you provide resources that transform the community.

Keep Reading